Flood Zones Explained: What Every New Construction Buyer in Lehigh Acres Must Know (2026)

Most of Lehigh Acres sits in minimal-risk Zone X — no mandatory flood policy on your mortgage. But the real Lehigh water story is rain and drainage, not surge. Here's how to read both.

You're shopping from two states away, and you've already braced yourself for the Florida flood-insurance horror story — the extra few thousand a year everybody warned you about before you can even move in. Then you start pulling Lehigh Acres listings, check the flood zones, and keep seeing the same two letters: Zone X. Minimal risk. No mandatory flood policy. And you assume you're reading it wrong, because that's not the Florida you were promised.

You're reading it right. Lehigh Acres is one of the reasons an out-of-state buyer can land brand-new construction in Southwest Florida without a mandatory flood insurance bill stapled to the mortgage. But "minimal risk on the map" and "you can ignore water entirely" are two different things — and the buyers who do great here understand the real Lehigh flood story, which has nothing to do with the ocean. Let's walk it the way somebody who sells here actually would.

In Lehigh, the Flood Zone Usually Reads One Letter: X

Here's what nobody explains. Every square foot of Lehigh Acres is in a flood zone — so is your current house, wherever you are. So is the White House. Everything is on FEMA's map. The question was never "is this home in a flood zone." It's which zone, and what FEMA actually thinks the odds are.

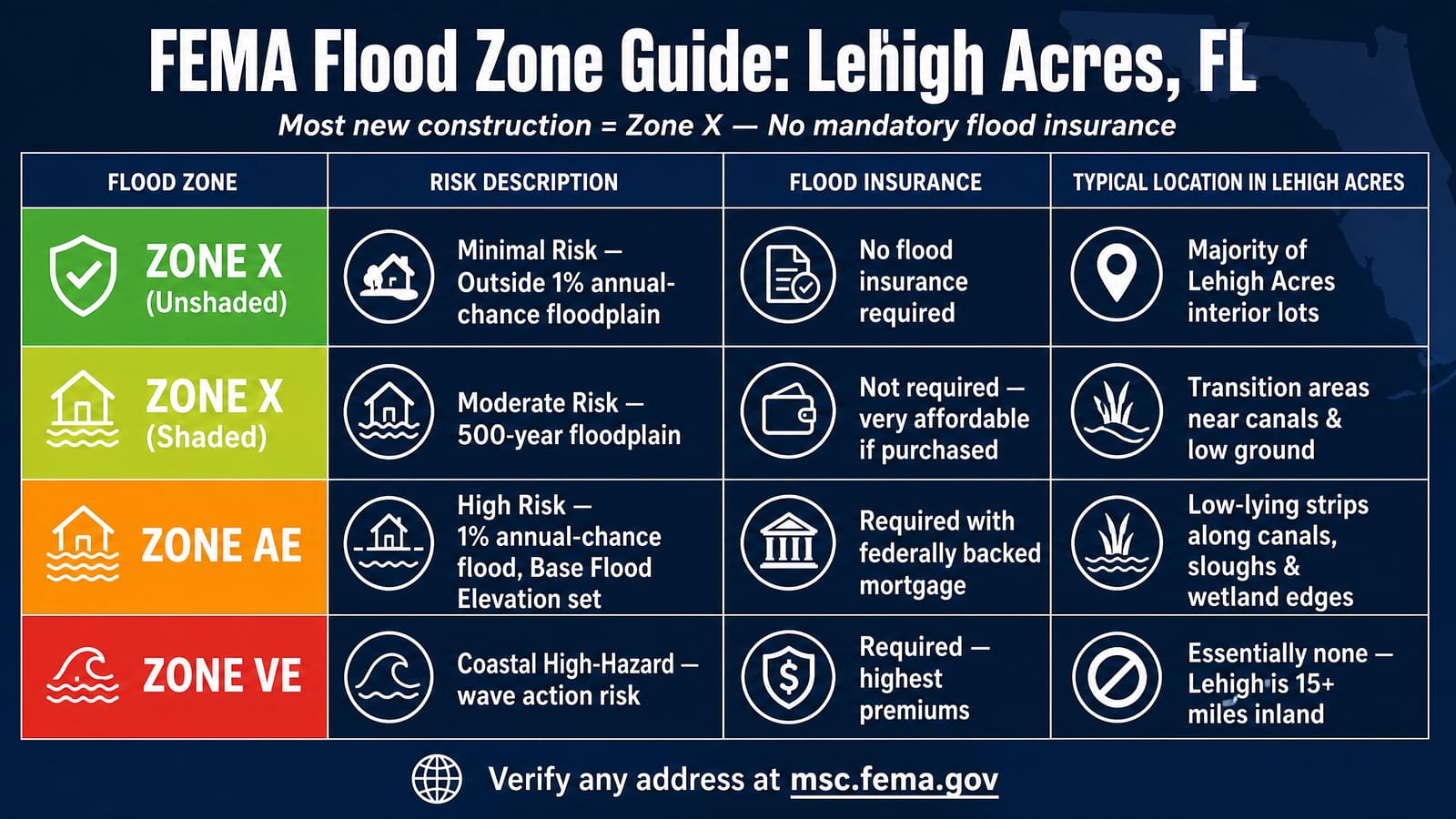

FEMA sorts the land into a few buckets that matter to you:

| Zone | What FEMA is saying | Flood insurance | Where it shows up in Lehigh Acres |

|---|---|---|---|

| X (unshaded) | Minimal risk — outside the 1%-annual-chance floodplain | Not federally required; cheap if you want it anyway | The majority of Lehigh's platted interior lots |

| X (shaded) | Moderate risk — the 0.2% (500-year) area | Not required; often very affordable | Transition areas near canals and low ground |

| AE | Special Flood Hazard Area — 1%-annual-chance flood, with a Base Flood Elevation set | Required with a federally backed mortgage | Low-lying strips along canals, sloughs, and wetland edges |

| VE | Coastal high-hazard — wave action | Required; priced highest | Essentially none — Lehigh is landlocked, ~15+ miles inland |

Here's where Lehigh is genuinely different from a coastal market like Cape Coral or Fort Myers Beach: most of it is Zone X. FEMA maps the bulk of Lehigh's interior lots as minimal risk — outside the high-risk floodplain, where a flood exceeding the base level is modeled as roughly a once-in-500-years event. There's no coastline, no storm surge zone, no VE. The AE zones that do exist are the low-lying edges — the strips that hug the canals, the natural sloughs, and the old wetland margins.

So is Lehigh a flood trap like the internet assumes every corner of Florida is? For most of it — no. And that's not a sales line, it's the map. That distinction is real, and it's money in your pocket.

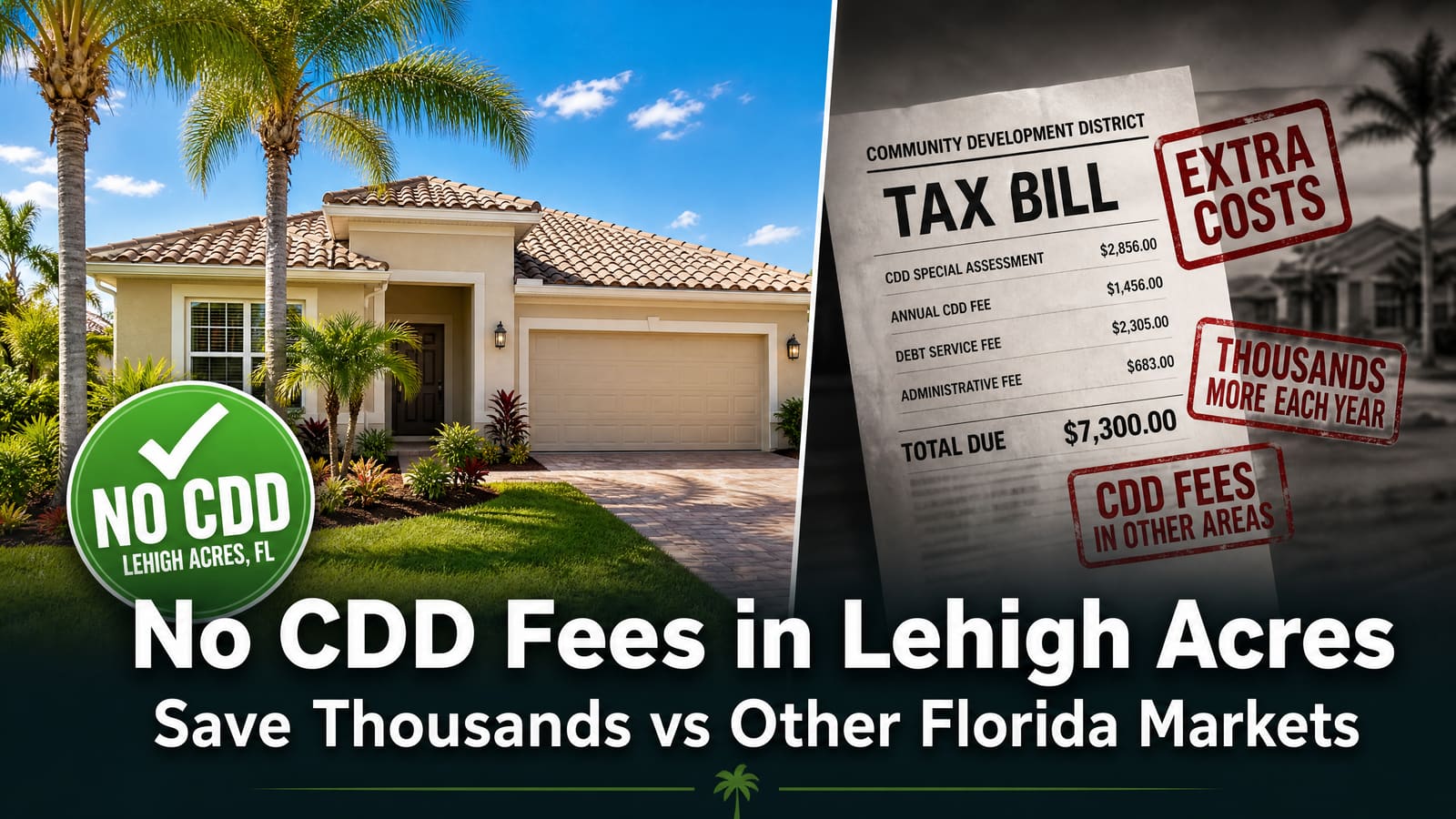

What Zone X Actually Puts in Your Pocket

Let's put a number on it, because this is the part out-of-state buyers underestimate.

In an AE or VE zone with a federally backed mortgage, flood insurance is mandatory — the lender requires it, every year, for as long as you owe. In Zone X, it's not federally required. On the majority of Lehigh's new construction, that's a line item that simply doesn't exist on your closing statement or your monthly payment. You can still buy a flood policy in Zone X if you want the peace of mind — and it's usually cheap, because the risk is low — but nobody's forcing it into your mortgage.

Run that forward the way you'd run any carrying cost. A mandatory flood policy in a coastal market can be a four-figure annual bill. Skipping it — legally, because your home is in a minimal-risk zone — is real money you keep every year you own the place, and real buying power a lender can count toward the house instead. That's a big piece of why Lehigh Acres stays the most affordable to actually own, not just to buy, new-construction market in Lee County.

The Real Flood Story Here Falls From the Sky, Not the Gulf

Now let me not sell you mush — because Lehigh has a genuine water story, and pretending otherwise is how people get surprised.

Lehigh's flood risk isn't the ocean. It's rain and drainage. This is flat, low-relief land with a high water table, platted back in the late 1950s and '60s as a giant grid — and in a hard Southwest Florida rainy season, or a slow-moving tropical system dumping a foot of water, the thing that keeps your street dry isn't elevation above the sea. It's how fast the water moves off the land.

That job belongs to the Lehigh Acres Municipal Services Improvement District (LA-MSID) — the local district (formerly the East County Water Control District) that runs the network of canals, weirs, and water-control structures threading through the community. When that system is working and your lot is graded right, water sheds and moves on. The homes that get into trouble are the low ones — old lots near a canal or a natural slough that sit close to grade, built decades ago before modern stormwater standards. That's the Lehigh flood reality, and "Zone X" doesn't make a low, poorly-graded lot immune to a bad afternoon in August.

Which is exactly where new construction earns its keep.

New Homes Are Built to Shed Water. The 1962 Ones Weren't.

A new home in Lehigh isn't just newer — it's engineered to handle water in ways the 1970s-plat house down the road never was.

Where a lot falls in an AE zone, new construction has to be built with its finished floor at or above the Base Flood Elevation, with Lee County's required freeboard on top — so the slab sits higher than the flood FEMA maps for it. And everywhere, a modern new-construction lot is graded and permitted to current stormwater standards: the pad is built up, the lot is shaped to drain toward the swales and the canal system, and the fill and elevation are done to code instead of to 1962 expectations. An older home on a low, flat lot can sit in the same Zone X and still take on water in a downpour simply because nobody engineered the grade. The new one is built to shed it.

And on the flood-insurance side, even in the minority of Lehigh homes that do land in an AE zone, FEMA's current Risk Rating 2.0 prices the policy on your specific home's elevation — so a new build sitting above BFE with an elevation certificate insures far cheaper than an old, low slab home in the same zone. Same two letters on the listing. Very different premium. (Lehigh is unincorporated Lee County, and Lee County's participation in FEMA's Community Rating System means SFHA homes here also get a community discount on that premium — a nice footnote, though for most Lehigh buyers the bigger win is simply not being in an SFHA at all.)

Don't Take My Word for It. Take FEMA's.

Don't take the listing's word for it either. It's public and it's fast, about two minutes.

Pull up FEMA's Flood Map Service Center (msc.fema.gov), type in the exact address, and you'll see that property's effective flood zone. If it comes back X, you've likely got no mandatory flood policy. If it comes back AE, ask the builder or your agent for the elevation certificate — the document showing how high the finished floor sits above Base Flood Elevation — so your insurance agent can quote the real, lower premium instead of a lazy zone-based guess.

Here's the local insight that matters more than the zone letter in Lehigh: look at where the lot sits, not just what the map says. The sections nearest the LA-MSID canals, the natural sloughs, and the lowest ground are the ones to scrutinize — that's where the AE pockets and the drainage headaches concentrate. The higher, drier interior blocks are where the easy Zone X new construction is. A five-minute look at the lot's elevation and its distance to the nearest canal tells you as much as the FEMA stamp does — and a new build that's been properly filled and graded is a different animal in a storm than an old low lot next door.

Listen Up: How to Use This When You Shop

Here's how to turn this into a smarter buy instead of trivia.

Don't over-worry the flood zone in Lehigh — but don't ignore water either. When you find a new build you like, do three things: check the zone on FEMA's map (most come back X), eyeball how low the lot is and how close it sits to a canal or slough, and if it's an AE lot, get the elevation certificate and a real flood quote on that home. On the majority of Lehigh new construction, you'll confirm what drew you here in the first place — minimal-risk ground, no mandatory flood policy, a home built and graded to shed water. That's a genuinely strong position, and most out-of-state buyers don't know Lehigh offers it.

What you should not do is either extreme: assume "it's Florida, so I'm doomed on flood insurance" (usually false here), or assume "Zone X means water can never touch me" (also false on a low, flat lot). The truth is in the middle, and it's in your favor if you check.

💡 Key Takeaways

- Most of Lehigh Acres is in Zone X — minimal flood risk, no federally mandated flood insurance — because it's landlocked, ~15+ miles inland, with no storm-surge or coastal VE zones.

- The AE (high-risk) zones that exist are the low-lying strips along canals, sloughs, and old wetland edges — the exceptions, not the rule.

- Lehigh's real flood risk is rainfall and drainage, not surge. Flat land and a high water table mean grading and the LA-MSID canal-and-weir system matter more than sea elevation.

- New construction is built up, graded, and permitted to current stormwater standards — and where it's in an AE zone, built at or above Base Flood Elevation with freeboard. Old low-lot homes weren't.

- Skipping a mandatory flood policy — legally, in a Zone X home — is real annual savings and real buying power a lender can count toward the house.

- Always verify the exact address on FEMA's Map Service Center, and in Lehigh, look at how low and how close to a canal the actual lot sits.

Frequently Asked Questions

What flood zone is most of Lehigh Acres in?

Most of Lehigh Acres' interior lots are in Zone X — minimal flood risk, outside the 1%-annual-chance floodplain — because the community is inland with no coastline. The higher-risk AE zones are limited to low-lying areas along canals, sloughs, and old wetland edges. There's essentially no VE (coastal) zone. Always confirm a specific address on FEMA's Flood Map Service Center.

Do I need flood insurance in Lehigh Acres?

Usually not. On the majority of Lehigh new construction — homes in Zone X — flood insurance is not federally required, so it won't be forced into your mortgage. You can still buy an affordable policy for peace of mind. If a home falls in an AE zone along a canal or low area, flood insurance is required with a federally backed mortgage, but a new build above Base Flood Elevation typically insures cheaply.

Is Lehigh Acres safe from flooding?

Its coastal-surge risk is very low — it's inland with no shoreline. Its real risk is localized rainfall flooding on flat, low-lying land during heavy storms, which is why drainage and lot grading matter so much here. The LA-MSID canal-and-weir system manages stormwater community-wide, and new construction is graded to modern standards to shed water. Older homes on low lots near canals are the ones most likely to see water.

Why is flooding a rainfall issue in Lehigh Acres instead of storm surge?

Lehigh is landlocked and roughly 15+ miles from the coast, so ocean storm surge doesn't reach it. What it has is flat terrain and a high water table, so the concern is heavy rain accumulating faster than it can drain. The Lehigh Acres Municipal Services Improvement District (formerly the East County Water Control District) maintains the canals and weirs that move that water off the land.

Can I buy new construction in Lehigh Acres without a flood insurance requirement?

Yes — in fact it's the norm. Most of Lehigh's new construction sits in minimal-risk Zone X, where flood insurance isn't federally required. Ask your agent to confirm the flood zone on any home you're considering; the majority will come back X, meaning no mandatory flood policy on your mortgage.

How do I check a specific home's flood zone in Lehigh Acres?

Go to FEMA's Flood Map Service Center at msc.fema.gov and enter the exact address to see its effective flood zone. In Lehigh, also look at how low the lot sits and how close it is to the nearest canal or slough — the low, canal-adjacent lots are where the AE pockets and drainage issues concentrate. For any AE-zone home, ask for the elevation certificate before getting an insurance quote.

See What's Actually Available

The market changes every week as homes list and close. See it live, filtered by what actually matters to you:

- Every active new build in Lehigh Acres

- New construction under $400K

- New construction under $350K

- Compare every builder in one place

Not sure whether the lot you love drains like a new build should, or sits low near a canal? That's the whole reason we're here.

If you need help buying in Lehigh Acres, call us at (239) 366-3996 and we'll pull the actual flood zone and eyeball the lot on any home you're eyeing — so you know exactly what you're buying before you fall in love or walk away.